Moderate strengthening of demand since August has buoyed the sagging air cargo market, but the seasonal surge in retail shipments for the holidays appears to be a third the normal level and more industry players are resetting expectations for a real recovery until the fall of 2024, or later.

Market intelligence provider Xeneta said airfreight volumes bumped up 2% in October from September and increased 2% year over year (y/y), but the sequential growth was subpar compared with peak seasons the previous five years. Midway through November, air cargo traffic remains barely ahead of last year’s disappointing fourth quarter, a compilation of surveys shows.

With consumer purchasing power stagnant amid nagging inflation and a cooling macroeconomic environment exacerbated by the new war between Israel and Hamas, a spending shift to services and experiences, few signs of significant retail restocking, and shippers favoring cheap ocean shipping, the freight sector now realizes air shipping probably won’t rally for at least another nine to 12 months.

Although airfreight volumes and rates have slowly leveled off since the double-digit declines to start the year and finally crossed over to growth, the annualized drop in cargo revenues during the third quarter reflects the uphill conditions faced by airlines and logistics providers.

Major U.S. and European airlines ranging from Air Canada to United Airlines, Air France-KLM and Lufthansa Group reported revenue declines of 25% to 40% for cargo during the three-month period, with the Lufthansa Cargo freighter unit barely breaking even. Korean Air’s cargo revenue fell 51%. Logistics behemoth Kuehne+Nagel said revenue for arranging air cargo moves dropped 46% y/y, while DSV said airfreight tonnage inched up from the second quarter but was down 14% versus the year-ago period.

“Most management teams to date have been tempering expectations for a better-than-expected peak season, and pushing out the timeline for freight recovery. Over the past several weeks, equities markets have largely reflected that sentiment, too,” said Bruce Chan, senior research analyst covering logistics at Stifel, in his monthly contribution to the Baltic Air Freight Index newsletter. “We continue to believe that demand will remain muted, capacity broadly abundant, and, while we may see some signs of episodic tightening from week-to-week or from lane-to-lane, the overall peak won’t offer much to write home about.”

The load factor, a measure of how full a passenger or freighter aircraft is, climbed to 59% in October but remained 2 points below last year’s level, according to Xeneta. Year to date, the fill rate is the lowest it’s been in five years, an indication of persistent weakness in the air cargo market.

The International Air Transport Association reinforced the sense of marginal growth with lagging numbers that showed a 1.9% increase in cargo traffic for September (Xeneta previously reported zero growth), the second month of y/y gains after a 19-month slide, despite global trade continuing to shrink.

For the full year to date, volumes are down about 8.5% versus 2022 and are 2% to 5% lower than January through October 2019, before COVID, according to various freight data firms.

Lackluster manufacturing reflects the widespread softening of global goods trade and lackluster transport demand, with the Purchasing Managers’ Index for new export orders still in contraction territory across major economies. And many retailers in earnings reports stated that spending on discretionary goods is slowing, with more household dollars being spent on essentials.

Worldwide tablet shipments, which predominantly move to market by air, posted a decline of 14.2% y/y in the third quarter, but that was up 18% from the previous quarter, according to preliminary data from the International Data Corp. Chromebook shipments also contracted for a y/y decline of 20.8%.

The recent upswing in air cargo demand, combined with slower growth in widebody passenger capacity as airlines shift to less intensive winter schedules, has led to improved shipping rates. Rising operating costs, such as jet fuel and labor, are also creating upward pricing pressure. The global average air cargo rate is about 23% lower, y/y, compared to 40% to 50% lower for much of 2023. Capacity is about 13% higher than a year ago.

Muted gains in global air cargo activity belie significant regional variation. Rates out of Asia, particularly south China, have accelerated since late summer as Chinese e-commerce marketplaces moved goods ahead of the Christmas season, according to logistics companies and price reporting agencies.

China-U.S. prices climbed 70% from early August to about $7.18/kg, according to the Freightos Air Index. In the past six weeks, Shanghai-North America rates increased 17%, pushing the year-to-date performance into positive territory for the first time. Rates on the Hong Kong-U.S. and Shanghai-U.S. lanes are now essentially at last year’s level. Two huge snow storms delayed operations at Alaska’s Anchorage airport this month, cutting cargo capacity and contributing to price inflation on trans-Pacific routes.

The Baltic Air Index, powered by TAC, shows rates from Hong Kong to North America increased about 13% since September, more than double the average sequential growth on those corridors over the last five years, excluding a drop in 2022.

Analysts note that the positive pricing has more to do with an easy comparison to last year at this time, when the market was tumbling from an incredible high, than from strong demand now. Last year at this time, demand was tumbling 12% from the highs of 2021. And some of October’s bump was attributed to the Golden Week holiday in China, as reopened factories pumped out more goods to make up for lost production time.

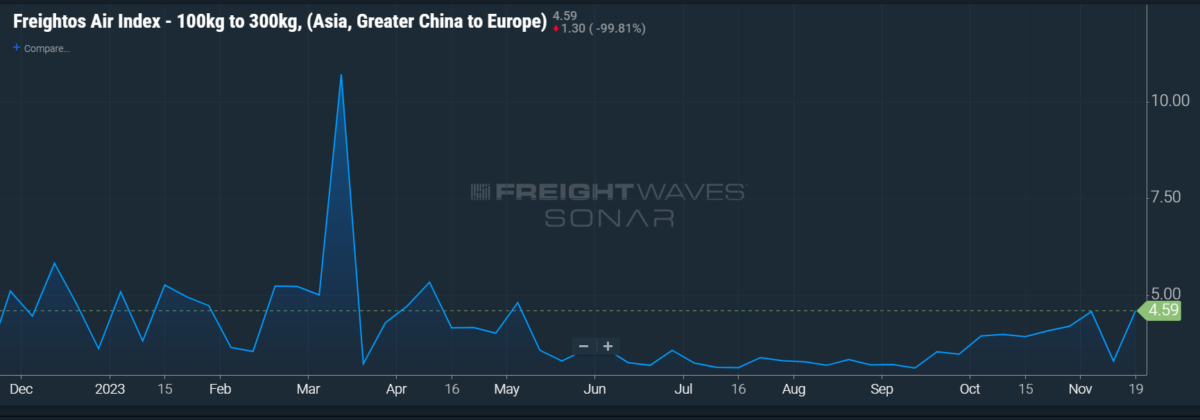

Meanwhile, rates on the China-Northern Europe trade lane recently fell 20%, back to their early September level, then rebounded 25% last week to $4.23/kg on more indications of demand improvement, especially from e-commerce shipments. Asia-Europe pricing is up more than 30% since mid-September.

The low-rate environment is spurring businesses to seek longer contracts by which they can lock in capacity at current pricing, while the freight forwarders they deal with are mostly seeking one-time shipping quotes from airlines on the spot market to get the lowest rate.

More evidence of underperformance this peak season comes from Morgan Stanely, which tracks domestic U.S. flight activity of parcel carriers. UPS and FedEx domestic flight counts increased in October from September, but less than normal. UPS flight utilization grew 4% versus 6% on average, slowing the y/y decline to 15% compared to 19% in September. FedEx flight activity increased 3% against an average seasonal gain of 7%. That was an improvement from the 9% sequential contraction in September and put the y/y decline at 6% versus minus 11% a month earlier.

UPS said in its third-quarter report that customers continued to shift volumes out of air to the ground, with average daily air volumes down 15.8% y/y.

Peak season underperforms

“What we’ve seen in September and coming into October, I would call a modest increase in the daily activity month over month. But nothing to the extent of what we would see in a historical pre-COVID peak cycle where you anticipate to see 30%-plus increases” for air and ocean demand, said Tim Robertson, CEO of DHL Global Forwarding, on an Oct. 24 conference call with reporters.

And increases in volumes during this year’s mini-peak season were mostly allocated to ocean shipping as shippers sought to take advantage of historically low container rates, according to logistics experts.

Ajay Virmani, CEO of Canadian all-cargo airline Cargojet, told analysts this month that e-commerce and other customers have indicated they expect similar volumes to last year’s disappointing peak season, during which the company’s volumes increased 10% to 15% in the fourth quarter from the prior three months.

Shipping containers with parcels are offloaded from a large freighter at DHL’s terminal at Dallas-Fort Worth airport. (Photo: Jim Allen/FreightWaves)

Robertson suggested that fourth-quarter volume gains could be muted because retailers are ordering earlier in the year to avoid potential supply chain bottlenecks and respond to more year-round interest from consumers.

“I think in the future, the concept of a single peak may be irrelevant. Rather we will see multiple peaks throughout the year, as your look at the rise of Prime days, fast fashion and continued developments in the e-commerce market,” said Robertson.

Many retailers are forecasting total merchandise will be flat this holiday season, but that revenues will be higher because of inflation and a higher mix of luxury goods sold, added Scott Surredin, the head of DHL Supply Chain, North America.

Any bump in late-year shipping volumes will likely be from retailers placing last-minute orders leading up to Black Friday and Cyber Monday to replenish stocks for a few specific products popular with consumers, DHL executives added.

During DHL Group’s recent earnings briefing, CEO Tobias Meyer said the company added a handful of charter flights in the trans-Pacific lane because of an unexpected spike in e-commerce volumes. The company is forecasting volumes for its Express business into the U.S. to be 14% higher than last year.

Equity analysts at Royal Bank of Canada said in a research note that they expect peak season to be flat versus last year, revising their previous assumption for modest freight growth across all modes and geographies.

Beyond pockets of increased air shipping, the air cargo sector still faces a long climb to real growth.

Strong U.S. growth of 4.9% during the third quarter could represent a high-water mark for the economy as the higher cost of borrowing resulting from Federal Reserve rate hikes on banks finally causes businesses and consumers to reduce spending, including for housing. And when people aren’t moving into new homes they aren’t buying furnishings, which impacts freight flows. Economists forecast growth could slow to an annual pace of 1.5% in the October-to-December period. A sign of the coming slowdown, Joseph Brusuelas, chief economist at RSM, told The Associated Press, was a 3.8% drop in business spending on new machinery and other equipment last quarter.

COVID stimulus money from the federal government, including through child care credits and student loan deferments, has also ended. More people are using up their savings or adding to personal debt, and defaults for auto and credit card loans are on the rise.

The global economy has weakened to its slowest pace in eight months, with the service sector losing steam. The International Monetary Fund last month said global GDP growth will tick down a 10th of a point to 2.9% in 2024.

S&P Global Market Intelligence forecasts tepid growth in trade in 2024, with U.S. seaborne imports expected to increase by just 2.3% y/y in the first quarter of 2024.

“Many of the forces driving U.S. economic growth in the third quarter will likely reverse in the coming quarters. While growth is strong, maintaining the current momentum will be very difficult in the year ahead. In Europe, the coming months will provide a clearer picture of whether the current economic challenges persist or evolve in 2024,” said Shawn DuBravac, chief economist at IPC, an Illinois-based trade association representing more than 3,000 members in the electronics industry, in the group’s latest outlook.

An emerging bright spot for airfreight companies is the huge demand for massive data centers that house IT infrastructure for delivering digital applications and services. “Every data center needs servers, blades and racks. Data centers continue to be constructed at a dizzying pace and now with the rise of AI, and quantum computing, we don’t see this going away anytime soon, which will have a knock on effect on air freight,” Brian Bourke, chief commercial officer at Seko Logistics, said during a media briefing last month.

Air carriers and freight forwarders have come to the realization that market conditions won’t significantly improve until well into the second half of 2024, said Niall van de Wouw, Xeneta’s chief airfreight officer.

Some ocean carriers say they don’t envision a meaningful freight recovery until 2025. “There are no clear data points showing that the restocking schedule will begin anytime soon, so it does not seem that a recovery will result from near-term growth in demand,” ZIM CFO Xavier Destriau recently said. If true, air carriers likely won’t see significant business improvement until later that year since shippers, absent any urgency to move goods, are expected to direct most new volumes to container lines.

0

0